PCB

PCB FPC

FPC Rigid-Flex

Rigid-Flex FR-4

FR-4 HDI PCB

HDI PCB Rogers High-Frequency Board

Rogers High-Frequency Board PTFE Teflon High-Frequency Board

PTFE Teflon High-Frequency Board Aluminum

Aluminum Copper Core

Copper Core PCB Assembly

PCB Assembly LED light PCBA

LED light PCBA Memory PCBA

Memory PCBA Power Supply PCBA

Power Supply PCBA New Energey PCBA

New Energey PCBA Communication PCBA

Communication PCBA Industrial Control PCBA

Industrial Control PCBA Medical Equipment PCBA

Medical Equipment PCBA Testing Service

Testing Service PCBA Testing Service

PCBA Testing Service Certification Application

Certification Application RoHS Certification Application

RoHS Certification Application REACH Certification Application

REACH Certification Application CE Certification Application

CE Certification Application FCC Certification Application

FCC Certification Application CQC Certification Application

CQC Certification Application UL Certification Application

UL Certification Application Transformers, Inductors

Transformers, Inductors High Frequency Transformers

High Frequency Transformers Low Frequency Transformers

Low Frequency Transformers High Power Transformers

High Power Transformers Conversion Transformers

Conversion Transformers Sealed Transformers

Sealed Transformers Ring Transformers

Ring Transformers Inductors

Inductors Wires,Cables Customized

Wires,Cables Customized Network Cables

Network Cables Power Cords

Power Cords Antenna Cables

Antenna Cables Coaxial Cables

Coaxial Cables Net Position Indicator

Net Position Indicator Solar AIS net position indicator

Solar AIS net position indicator Capacitors

Capacitors Connectors

Connectors Diodes

Diodes Embedded Processors & Controllers

Embedded Processors & Controllers Digital Signal Processors (DSP/DSC)

Digital Signal Processors (DSP/DSC) Microcontrollers (MCU/MPU/SOC)

Microcontrollers (MCU/MPU/SOC) Programmable Logic Device(CPLD/FPGA)

Programmable Logic Device(CPLD/FPGA) Communication Modules/IoT

Communication Modules/IoT Resistors

Resistors Through Hole Resistors

Through Hole Resistors Resistor Networks, Arrays

Resistor Networks, Arrays Potentiometers,Variable Resistors

Potentiometers,Variable Resistors Aluminum Case,Porcelain Tube Resistance

Aluminum Case,Porcelain Tube Resistance Current Sense Resistors,Shunt Resistors

Current Sense Resistors,Shunt Resistors Switches

Switches Transistors

Transistors Power Modules

Power Modules Isolated Power Modules

Isolated Power Modules AC-DC Power Modules

AC-DC Power Modules DC-AC Module(Inverter)

DC-AC Module(Inverter) RF and Wireless

RF and WirelessHow to Calculate and Reduce Scrap Cost in PCB Manufacturing?

2026-01-19

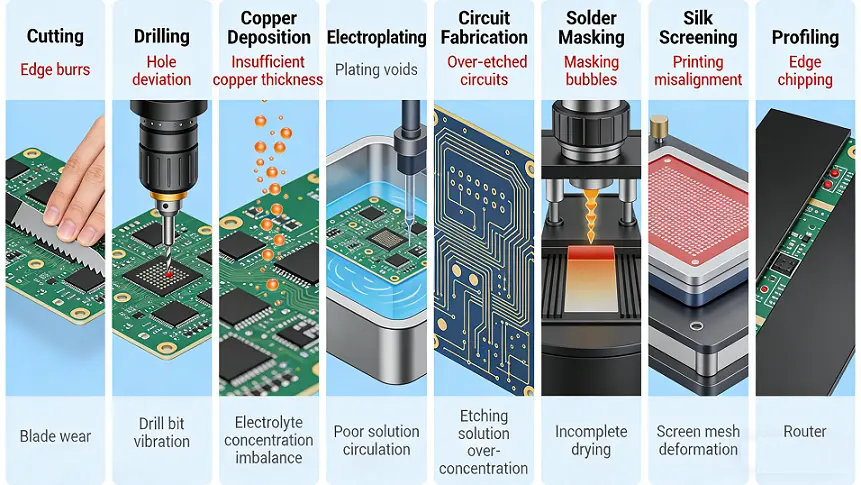

SCRap cost is one of the core indicators affecting enterprises' profitability, production efficiency, and market competitiveness. The PCB production process is complex, covering dozens of procedures such as copper-clad laminate cutting, drilling, copper deposition, electroplating, circuit fabrication, solder masking, silk screening, and profiling. Each procedure may result in product scrap due to factors like material defects, insufficient equipment precision, operational errors, and environmental fluctuations. According to industry data, the scrap rate of maturePCB enterprises is usually controlled between 2% and 5%, while that of small and medium-sized enterprises or complex PCBs (such as High-Density Interconnect (HDI) boards and blind/buried hole boards) may reach as high as 8% to 12%. Excessively high scrap costs not only erode enterprise profits but also cause capacity waste, delivery delays, and even undermine customer trust.

Accurately calculating scrap cost is the premise of cost control, and systematically reducing the scrap rate is key to enterprises' cost reduction and efficiency improvement. Starting from the calculation logic, constituent elements, and core causes of scrap cost, this article elaborates on the accurate accounting method of scrap cost in conjunction with the entire PCB production process, and proposes actionable reduction strategies, providing professional and comprehensive cost control solutions for PCB manufacturing enterprises.

I. Core Definition and Calculation Logic of PCB Scrap Cost

PCB scrap cost refers to the sum of all direct and indirect costs incurred during the PCB production process when products fail to meet design requirements, quality standards, or are irreparable. Unlike a single material loss cost, scrap cost covers a broader scope, including both explicit direct costs and implicit indirect costs. If only explicit costs are accounted for, the scrap loss will be underestimated, which in turn impairs the scientificity of cost control decisions.

(I) Constituent Elements of Scrap Cost

The composition of PCB scrap cost can be divided into two categories: direct costs and indirect costs. Each category includes multiple sub-items, which need to be sorted out and accounted for one by one to ensure no omissions.

1. Direct Costs: Costs directly asSOCiated with scrapped products and quantifiable, serving as the core component of scrap cost.

(1) Material Costs: The most intuitive scrap cost, including the costs of various materials consumed in the production process, such as copper-clad laminates (CCL), copper foil, solder mask ink, silk screen ink, dry film, chemical agents (copper deposition solution, electroplating solution, etching solution, etc.), drill bits, and backing plates. The accounting of material costs should be based on the quantity, specifications, and unit price of scrapped products. For example, the unit price of an FR-4 copper-clad laminate with specifications of 500mm×600mm and thickness of 1.6mm is 80 yuan. If 10 pieces of this specification are scrapped after cutting, the material cost loss alone amounts to 800 yuan, and the costs of ink, dry film, and other materials consumed in subsequent procedures should also be included.

(2) Processing Costs: Costs such as labor costs, equipment depreciation costs, and energy consumption costs incurred by scrapped products during production. Labor costs are calculated based on the hourly wage of the corresponding procedure and the actual working hours invested. For example, if the hourly wage of workers in the drilling procedure is 30 yuan, and the actual working hours invested in a batch of scrapped products is 20 hours, the corresponding labor cost loss is 600 yuan. Equipment depreciation costs are allocated based on the original equipment value, service life, and daily output. For example, a drilling machine with an original value of 1.2 million yuan, a service life of 10 years, 300 working days per year, and a daily output of 500 PCBs has a depreciation cost of 0.8 yuan per PCB. If 100 pieces are scrapped, the depreciation cost loss is 80 yuan. Energy consumption costs include electricity and water consumption, accounted for based on actual consumption and unit prices during production.

2. Indirect Costs: Costs indirectly incurred due to product scrap, which are difficult to quantify directly but actually exist. Such costs are easily overlooked but exert a significant impact on enterprise profits after long-term accumulation.

(1) Capacity Waste Costs: Scrapped products occupy production capacity resources such as equipment, workshops, and labor, reducing the output of qualified products within the same period and thus causing the loss of potential output benefits. For example, if a production line has a daily capacity of 1,000 PCBs but only produces 900 qualified pieces due to an excessively high scrap rate, the marginal profit corresponding to the missing 100 qualified products constitutes the capacity waste cost.

(2) Rework and Re-inspection Costs: Some defective products will undergo rework attempts. If they still fail to meet standards and are scrapped after rework, the labor, materials, and equipment costs consumed during rework should be included in scrap costs. Meanwhile, re-inspection costs incurred to identify defects and confirm scrap causes (such as AOI testing, X-Ray testing, and microscopic observation) should also be incorporated into the accounting.

(3) Delivery Delay Costs: Insufficient capacity caused by product scrap may lead to order delivery delays, resulting in liquidated damages, customer churn risk costs, urgent replenishment costs, etc. For example, if an order is delayed by 3 days due to an excessive scrap rate, liquidated damages of 1% of the order amount (assuming an order amount of 100,000 yuan, equivalent to 1,000 yuan) must be paid in accordance with the contract. Additionally, additional overtime costs and energy consumption costs for urgent equipment operation incurred for expedited replenishment should also be included.

(4) Management and Quality Costs: Including labor costs of quality control personnel, defect analysis costs, quality improvement investment costs (such as equipment calibration, process optimization, and employee training), as well as additional costs for quality system audits and customer complaint handling caused by excessively high scrap rates.

(II) Accurate Calculation Method of Scrap Cost

The calculation of PCB scrap cost must adhere to the principle of "full process and full elements", and a standardized accounting formula and data statistics system should be established to avoid deviations caused by inconsistent accounting standards. The following is a general calculation framework, which enterprises can adjust according to their own production scale and product types.

1. Calculation Formula for Single Batch Scrap Cost:

Single Batch Scrap Cost = Direct Material Cost + Direct Processing Cost + Indirect Cost

(1) Direct Material Cost = Σ (Unit Consumption of a Material × Scrap Quantity × Unit Price of Material)

Among them, unit material consumption should be determined based on product specifications and production processes. For example, each 1.6mm-thick FR-4 PCB consumes 0.32㎡ of copper-clad laminate and 0.05kg of solder mask ink.

(2) Direct Processing Cost = Labor Cost + Equipment Depreciation Cost + Energy Consumption Cost

Labor Cost = Working Hours Invested in Each Procedure × Hourly Wage of Corresponding Procedure;

Equipment Depreciation Cost = Scrap Quantity × Equipment Depreciation Allocation per Unit Product;

Energy Consumption Cost = Actual Energy Consumption of Each Procedure × Energy Consumption Unit Price.

(3) Indirect Cost = Capacity Waste Cost + Rework and Re-inspection Cost + Delivery Delay Cost + Management and Quality Cost

Capacity Waste Cost = Scrap Quantity × Marginal Profit per Qualified Product;

Rework and Re-inspection Cost = Rework Hours × Hourly Wage + Re-inspection Equipment Depreciation + Re-inspection Material Consumption;

Delivery Delay Cost = Liquidated Damages + Additional Costs for Urgent Replenishment;

Management and Quality Cost = Working Hours Invested by Quality Personnel × Hourly Wage + Defect Analysis Fees + Quality Improvement Investment.

2. Monthly/Annual Scrap Cost Accounting:

Monthly Scrap Cost = Σ Scrap Costs of Each Batch + Monthly Fixed Quality Control Costs (such as quality training, daily equipment calibration, etc.);

Annual Scrap Cost = Σ Monthly Scrap Costs + Annual Quality System Investment Costs + Annual Indirect Costs of Customer Churn.

3. Linked Accounting of Scrap Rate and Unit Scrap Cost:

Scrap Rate = (Scrap Product Quantity ÷ Total Production Quantity) × 100%;

Unit Scrap Cost = Total Scrap Cost ÷ Total Production Quantity;

II. Analysis of Scrap Causes and Cost Proportion in Each PCB Production Procedure

The PCB production process is lengthy. Different procedures have distinct process characteristics, equipment requirements, and quality control points, resulting in significant differences in scrap causes and cost proportions. Clarifying the core causes of scrap in each procedure is crucial for formulating targeted reduction strategies and achieving precise control. Combined with industry practices, the scrap causes and cost proportions of each main procedure are as follows:

II. Analysis of Scrap Causes and Cost Proportion in Each PCB Production Procedure

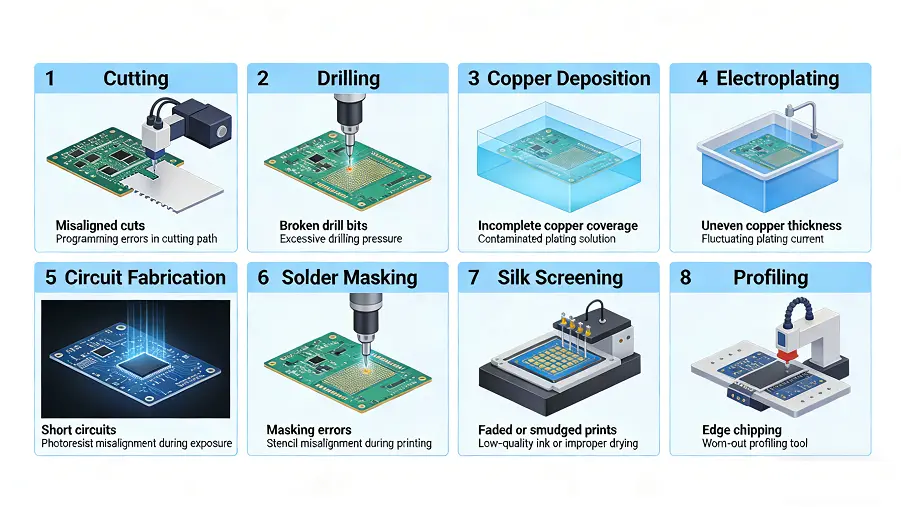

1. Cutting Procedure: Mainly cuts copper-clad laminates to meet the specification requirements of subsequent procedures. The main causes of scrap include: inherent defects of copper-clad laminates (such as warpage, surface scratches, and copper foil peeling), insufficient precision of cutting equipment (such as blade wear and positioning deviation), and operational errors (such as incorrect size setting and placement offset), leading to oversized cut sheets, excessive edge burrs, sheet damage, etc. The scrap cost of this procedure is mainly the material cost of copper-clad laminates, accounting for more than 70% of the total scrap cost of the procedure.

(I) Preliminary Procedures: Cutting and Drilling (Scrap Cost Proportion: 15%-20%)

1. Cutting Procedure: Mainly cuts copper-clad laminates to meet the specification requirements of subsequent procedures. The main causes of scrap include: inherent defects of copper-clad laminates (such as warpage, surface scratches, copper foil peeling), insufficient precision of cutting equipment (such as blade wear, positioning deviation), and operational errors (such as incorrect size setting, placement offset), leading to excessive size of cut sheets, excessive edge burrs, sheet damage, etc. The scrap cost of this procedure is mainly the material cost of copper-clad laminates, accounting for more than 70% of the scrap cost of this procedure.

2. Drilling Procedure: As one of the core procedures in PCB production, it involves drilling through holes, blind holes, buried holes, etc., on the sheet. The causes of scrap are relatively complex, including: drill bit wear and breakage leading to hole position deviation, excessive hole diameter, and rough hole walls; poor quality of backing plates resulting in hole edge burrs and hole wall contamination; positioning datum deviation causing hole position offset beyond the allowable range; improper setting of drilling parameters (such as unreasonable rotation speed and feed rate) leading to hole wall delamination and resin smearing. Scrap in the drilling procedure not only involves the cost of copper-clad laminates but also includes the cost of consumables such as drill bits and backing plates, as well as secondary scrap caused by hole wall defects in the subsequent copper deposition procedure, accounting for a relatively high proportion of costs.

(II) Middle Procedures: Copper Deposition, Electroplating, and Circuit Fabrication (Scrap Cost Proportion: 40%-50%)

Middle procedures are key links for the formation of PCB electrical performance, featuring high process complexity and strict requirements on the environment, chemical agents, and equipment precision, making them the link with the highest scrap cost.

1. Copper Deposition Procedure: Forms a thin copper layer on the hole wall through chemical deposition to achieve hole wall conductivity. The main causes of scrap include: unbalanced chemical agent concentration, excessive temperature fluctuation, and improper control of copper deposition time leading to no copper on the hole wall, poor copper layer adhesion, and hole wall voids; inadequate cleaning of oil stains and impurities on the sheet surface, affecting copper deposition results; uneven stirring of equipment causing uneven copper layer thickness. Once scrapped in this procedure, the sheet is difficult to repair and must be directly scrapped, with costs including the sheet, chemical agents, and preliminary processing costs.

2. Electroplating Procedure: Plates a copper layer on the surface and hole wall of the sheet after copper deposition to enhance conductivity and wear resistance. The causes of scrap include: abnormal concentration, pH value, and temperature of the electroplating solution leading to excessive or insufficient copper layer thickness, rough copper layer, pinholes, and pitting; poor contact of hangers resulting in local non-plating; incorrect setting of electroplating time leading to non-compliant copper layer thickness; impurities mixed into the electroplating solution causing plating defects. In addition to material costs, the scrap cost of this procedure also includes electroplating energy consumption and equipment depreciation costs, accounting for about 30% of the scrap cost of middle procedures.

3. Circuit Fabrication Procedure: Fabricates PCB circuits through dry film exposure, development, and etching processes. The main causes of scrap are: loose dry film adhesion, bubbles, and scratches leading to circuit short circuits and open circuits; improper setting of exposure parameters (such as insufficient or excessive exposure time and energy) resulting in blurred circuits and low resolution; abnormal concentration and temperature of the developer causing incomplete or over-development; improper control of etching solution concentration and speed leading to uneven circuit etching, residue, or over-etching. The circuit fabrication procedure is a high-incidence link for PCB scrap. Especially for high-density PCBs with small circuit spacing and thin line width, minor defects can lead to product scrap, accounting for more than 40% of the scrap cost of middle procedures.

(III) Post Procedures: Solder Masking, Silk Screening, Shaping, and Testing (Scrap Cost Proportion: 25%-30%)

Post procedures are mainly responsible for PCB surface protection, marking printing, shape processing, and performance testing. The causes of scrap are mostly related to operational precision and material quality.

1. Solder Masking Procedure: Coats the PCB surface with solder mask ink to protect the circuit from oxidation, contamination, and mechanical damage. The causes of scrap include: bubbles, pinholes, and sagging of solder mask ink leading to circuit exposure; improper exposure and development parameters resulting in solder mask opening deviation, blocking pads or exposing circuits; poor ink adhesion causing peeling. The scrap cost of this procedure is mainly ink cost and rework cost.

2. Silk Screening Procedure: Prints component marks, models, polarities, and other information. The causes of scrap include: wear and blockage of silk screen stencils leading to blurred patterns and broken lines; improper ink ratio causing easy peeling and bleeding after printing; positioning deviation resulting in incorrect mark positions, affecting component assembly. Most scrap in the silk screening procedure can be repaired by rework, but if it still fails to meet standards after rework, it should be included in scrap costs.

3. Profiling Procedure: Processes the PCB into the final shape and size through routing, stamping, and other methods. The causes of scrap include: tool wear and positioning deviation leading to oversized profiles and edge burrs; excessive stamping pressure causing sheet damage and circuit breakage; unreasonable shape design resulting in stress concentration and sheet warpage after profiling. The scrap cost of this procedure includes sheet cost and tool wear cost.

4. Testing Procedure: Tests the electrical performance of PCBs (such as continuity, insulation resistance, and impedance) to screen out unqualified products. The main cause of scrap is defects left by previous procedures (such as circuit short circuits, open circuits, and no copper on hole walls). The scrap cost of this procedure is the cumulative cost of all previous procedures, and if batch defects are found in testing, the loss will increase significantly.

(IV) Other Causes: Environment, Management, and Design (Scrap Cost Proportion: 5%-10%)

In addition to process defects in each procedure, environmental fluctuations, improper management, and unreasonable design can also lead to scrap. In terms of the environment: improper temperature and humidity control (such as excessive humidity causing sheet moisture absorption and low humidity leading to dry film brittleness), and excessive workshop dust resulting in surface contamination. In terms of management: non-standard employee operations, insufficient training, lack of quality inspection processes, and inadequate daily equipment maintenance. In terms of design: excessively small circuit spacing, mismatched hole diameter and pad, insufficient process margin, etc., leading to difficulty in quality control during production and increased scrap risk.

III. Systematic Strategies for Reducing PCB Scrap Cost

Reducing PCB scrap cost needs to start from three dimensions: "source prevention, process control, and terminal improvement". Combined with the scrap causes of each procedure, a full-process and multi-level control system should be established. It is necessary to specifically address defect problems in individual procedures and optimize the overall production management and quality control system to achieve a dual reduction in scrap rate and scrap cost.

(I) Source Prevention: Reducing Inherent Risks from Design, Materials, and Equipment

Source prevention is the most effective means to reduce scrap cost. By optimizing design, strictly controlling material quality, and upgrading equipment precision, the possibility of defects is fundamentally reduced.

1. Optimizing PCB Design to Improve Process Feasibility: The PCB design stage must fully consider production process characteristics to avoid scrap caused by unreasonable design. Specific measures include: reasonably setting circuit spacing and line width, and reserving sufficient process margin (such as circuit spacing not less than 0.1mm, which can be appropriately reduced for high-precision equipment but must be confirmed with the production department in advance); optimizing the matching relationship between hole diameter and pad to avoid drilling and electroplating defects caused by excessively small or large hole diameters; reducing the complexity of blind and buried holes, and reasonably planning the layer structure to lower production difficulty; adding positioning datums and foolproof marks to facilitate positioning and operation in subsequent procedures. Meanwhile, after design completion, a process review should be organized by the design, production, and quality departments to identify potential design hazards and ensure the design scheme meets production capacity.

2. Strictly Controlling Material Quality to Reduce Defects from the Source: Material quality is the foundation of PCB quality, and a rigorous supplier access and material inspection system must be established. Measures include: selecting qualified and reputable suppliers (such as well-known brands like Shengyi and Kingboard for copper-clad laminates), signing quality agreements, and clarifying material quality standards and claim clauses; establishing an incoming material inspection process to conduct sampling or full inspection on key materials such as copper-clad laminates, copper foil, ink, dry film, and chemical agents. Inspection items include dimensional accuracy, surface quality, and performance parameters (such as the dielectric constant of copper-clad laminates and copper foil adhesion). Unqualified materials are strictly prohibited from being put into storage; strengthening material storage management, controlling warehouse temperature and humidity to prevent material moisture absorption, deterioration, and warpage. For consumables (such as drill bits and dry film), store them in separate areas and take moisture-proof and dust-proof measures.

3. Upgrading Equipment Precision to Improve Process Stability: Equipment precision directly affects production process stability and product quality. It is necessary to timely upgrade equipment or perform precision calibration according to production needs. Specific measures include: introducing high-precision equipment (such as CNC drilling machines, laser drilling machines, and high-precision exposure machines) for core procedures such as drilling and circuit fabrication to improve hole position precision and circuit resolution; regularly maintaining, servicing, and calibrating equipment precision (such as weekly calibration of drilling machine positioning precision and monthly calibration of exposure machine energy), establishing equipment maintenance records to document maintenance time, content, and calibration results; replacing aging and worn equipment parts (such as drill bits, blades, and hangers) to avoid product defects caused by part wear; introducing automated equipment (such as automatic cutting machines, automatic film laminators, and automatic testing equipment) to reduce manual operation errors and improve production consistency.

(II) Process Control: Optimizing Processes, Strengthening Operations, and Strictly Inspecting to Reduce Process Defects

Process control is the core link to reduce scrap cost. By optimizing process parameters, standardizing operation processes, and strengthening full-process inspection, defects are detected and addressed in a timely manner to avoid final scrap caused by defect accumulation.

1. Optimizing Process Parameters to Improve Process Stability: For the process characteristics of each procedure, optimize parameter settings through experiments and establish standardized process documents to ensure the production process is standardized and controllable. For example, in the drilling procedure, optimize parameters such as rotation speed, feed rate, and drill bit model according to copper-clad laminate thickness and hole diameter to reduce hole wall delamination and burrs; in the copper deposition and electroplating procedures, strictly control parameters such as chemical agent concentration, temperature, time, and stirring speed, regularly test agent performance, and timely supplement or replace agents to avoid plating defects caused by parameter fluctuations; in the circuit fabrication procedure, optimize parameters such as exposure energy, development time, and etching speed to ensure clear circuits and no residue. Meanwhile, incorporate optimized process parameters into standard operating procedures (SOP) and require employees to strictly implement them, prohibiting unauthorized parameter modifications.

2. Standardizing Operation Processes and Strengthening Employee Training: The standardization of employee operations directly affects product quality, and a sound operation training and assessment system must be established. Measures include: formulating standardized operating procedures (SOP) for each procedure, clarifying operation steps, precautions, and quality control points to ensure each employee operates in accordance with standards; regularly organizing employee training covering process knowledge, equipment operation, defect identification, emergency handling, etc. For new employees, conduct pre-job training and practical assessments, and only allow them to take up posts after passing; carry out skill competitions and technical disclosure meetings to improve employees' operational skills and quality awareness; establish an operation responsibility traceability system, clarify the responsible party for scrap caused by operational errors, and analyze causes to formulate improvement measures.

3. Establishing a Full-Process Inspection System to Timely Detect Defects: Through a three-level inspection system of "first article inspection + in-process patrol inspection + finished product full inspection", defects are detected and handled in a timely manner to prevent defects from flowing into the next procedure and reduce subsequent cost losses. Specific measures include: first article inspection, manufacturing the first article before mass production of each batch, and having quality personnel test indicators such as size, appearance, and electrical performance to confirm qualification before mass production; in-process patrol inspection, with quality personnel conducting regular sampling inspections on each procedure, focusing on high-incidence defects (such as hole position deviation in drilling, circuit short circuits and open circuits, and solder mask opening deviation), and immediately stopping production to investigate and adjust process parameters or equipment when problems are found; finished product full inspection, adopting a combination of manual inspection and automated testing equipment to inspect the appearance, size, and electrical performance of finished PCBs. Automated testing equipment (such as AOI, X-Ray, and flying probe testers) can improve inspection efficiency and precision, detecting minor defects that are difficult to find manually (such as hole wall voids and inner layer circuit short circuits); establish a defect traceability system, record defect types, quantities, originating procedures, and causes, regularly analyze defect data to identify high-incidence defects and key control points, and optimize them in a targeted manner.

4. Controlling the Production Environment to Reduce Environmental Impact: PCB production has high requirements on environmental temperature, humidity, and cleanliness, and an environmental control system must be established. Measures include: controlling workshop temperature and humidity within a reasonable range (such as 22±2℃ and 55±5%RH), installing temperature and humidity monitoring equipment for real-time monitoring and automatic adjustment; strengthening workshop cleanliness management, regularly conducting dust cleaning and air purification, and adopting clean workshops for key procedures such as drilling and circuit fabrication to avoid defects caused by dust contamination; implementing effective moisture-proof and anti-static measures in the workshop to prevent sheet moisture absorption and circuit damage due to static electricity.

(III) Terminal Improvement: Defect Rework, Data Analysis, and Continuous Optimization to Reduce Loss Expansion

Terminal improvement mainly targets generated defective products and scrap data. Through reasonable rework and in-depth data analysis, loss expansion is reduced, and the production process is continuously optimized to avoid repeated occurrence of similar defects.

1. Conducting Reasonable Rework and Repair to Reduce Direct Scrap: For repairable defective products, rework should be organized in a timely manner to avoid direct scrap and reduce cost losses. A rework evaluation process needs to be established: quality personnel inspect defective products to determine defect type, severity, and repairability; for repairable defects (such as blurred silk screen, solder mask bubbles, and minor burrs), formulate a special rework plan, clarify rework procedures, operation methods, and quality standards, and arrange professional personnel to perform rework; re-inspect after rework, and only allow qualified products to flow into the next procedure, otherwise handle them as scrap. Meanwhile, count rework costs, analyze rework causes, optimize the production process, and reduce rework frequency.

2. Conducting In-depth Analysis of Scrap Data to Precisely Locate Improvement Directions: Establish a scrap data statistical analysis system, summarize and analyze scrap data regularly (daily, weekly, monthly), explore scrap causes, and formulate targeted improvement measures. Analysis content includes: scrap rate of each procedure, proportion of scrap cost, distribution of defect types, causes of high-incidence defects, and responsible departments/personnel; through trend analysis, judge the change trend of scrap rate and evaluate the effectiveness of improvement measures; compare scrap data of different batches and products to identify batch and regular defects, and optimize processes or designs. For example, if hole position deviation defects in the drilling procedure are found to be high-incidence, investigate factors such as equipment positioning precision, drill bit quality, and operation specifications, and conduct targeted equipment calibration, drill bit replacement, and strengthened operation training.

3. Establishing a Continuous Improvement Mechanism to Form Closed-Loop Management: Combined with the results of scrap data analysis, establish a continuous improvement mechanism (such as the PDCA cycle) to ensure the implementation of improvement measures and form a closed-loop management of "problem identification—cause analysis—measure formulation—improvement implementation—effect verification—consolidation and optimization". Measures include: setting up a quality improvement team composed of personnel from production, technology, and quality departments to carry out special improvement projects for high-incidence scrap defects; regularly holding quality analysis meetings to report scrap data and improvement progress, and solve problems encountered in the improvement process; incorporating effective improvement measures into standardized process documents and operation procedures to consolidate improvement results; holding accountable for links with ineffective improvement and urging rectification.

(IV) Management Optimization: Improving Systems, Strengthening Assessment, and Cooperating Collaboratively to Enhance Control Capability

A sound management system is the guarantee for reducing scrap cost. By improving the quality control system, strengthening assessment and incentives, and enhancing departmental collaboration, the overall cost control capability of the enterprise is improved.

1. Improving the Quality Control System and Establishing Standardized Management: Introduce quality management systems such as ISO9001 and IATF16949, and establish a full-process quality control system covering design, procurement, production, inspection, and delivery; formulate quality management systems, clarify the quality responsibilities of each department and position to ensure no dead corners in quality control; establish a quality traceability system, record the production process, material source, and inspection results of each batch of products to facilitate rapid traceability and cause investigation when problems occur; regularly conduct quality system audits, identify system loopholes, and optimize and improve them in a timely manner.

2. Strengthening Assessment and Incentives to Improve Overall Quality Awareness: Establish an assessment and incentive mechanism linked to scrap rate and scrap cost, and assign cost control responsibilities to each department and employee. Measures include: incorporating scrap rate and unit scrap cost into the performance assessment indicators of production and quality departments, setting reasonable target values (such as controlling the scrap rate within 3%), providing rewards for exceeding targets, and imposing penalties for failing to meet targets; offering special rewards to employees who identify batch defects and put forward effective improvement suggestions to stimulate the enthusiasm of all employees to participate in quality control; regularly conducting quality training and publicity activities to strengthen the quality awareness of all employees and establish the concept of "quality first, cost reduction and efficiency improvement".

3. Strengthening Departmental Collaboration to Form Control Synergy: Reducing scrap cost requires the collaborative cooperation of multiple departments such as design, procurement, production, technology, quality, and finance to avoid working in isolation. For example, the design department strengthens communication with the production department to ensure the design scheme meets production capacity; the procurement department collaborates with the quality department to strictly control material quality and timely handle unqualified materials; the production department cooperates with the technology department to optimize process parameters and solve technical problems in the production process; the quality department collaborates with the finance department to accurately account for scrap cost and provide data support for improvement measures. Regularly hold cross-departmental coordination meetings to report the work progress of each department, solve problems encountered in the collaboration process, and form control synergy.

IV. Implementation Guarantee and Precautions for Scrap Cost Control

Reducing PCB scrap cost is a long-term and systematic task. A sound implementation guarantee mechanism must be established, and common misunderstandings in the control process must be avoided to ensure the effective implementation of control measures and the continuous reduction of scrap cost.

(I) Implementation Guarantee Mechanism

1. Organizational Guarantee: Establish a special cost control team led by the enterprise leader, with members including the heads of production, technology, quality, procurement, finance, and other departments. Clarify the team's responsibilities, coordinate and promote scrap cost control work, regularly hold work meetings, track improvement progress, and solve major problems.

2. Financial Guarantee: Arrange reasonable capital investment for equipment upgrading, automation transformation, introduction of quality testing equipment, employee training, process optimization, etc., to provide financial support for cost control; at the same time, invest a certain proportion of the savings from scrap cost into subsequent control work to form a virtuous cycle.

3. Technical Guarantee: Establish a technical R&D team focusing on PCB process optimization, defect improvement, new material application, etc., to provide technical support for cost control; strengthen cooperation with universities, scientific research institutions, and industry associations to introduce advanced technologies and management experiences and improve the enterprise's control level.

4. Data Guarantee: Establish an information management system (such as MES production management system and ERP resource planning system) to realize information-based control of the production process, scrap data, and cost accounting, automatically collect, summarize, and analyze data, improve data accuracy and analysis efficiency, and provide a reliable basis for decision-making.

(II) Control Precautions

1. Avoid Overpursuing Low Scrap Rate While Ignoring Cost Balance: Reducing the scrap rate requires a certain amount of investment (such as equipment upgrading, material premium, and inspection fees). It is necessary to comprehensively account for input and output, and avoid excessive investment to pursue an extremely low scrap rate, which may lead to a decline in overall profits. For example, for ordinary consumer PCBs, controlling the scrap rate within 3%-4% can achieve optimal cost-effectiveness, and there is no need to invest excessive funds to reduce the scrap rate to below 1%.

2. Avoid Focusing Only on Explicit Costs While Ignoring Implicit Costs: In the process of cost accounting and control, both direct and indirect costs must be fully considered, especially implicit costs such as delivery delay costs, capacity waste costs, and customer churn costs, to avoid control decision deviations caused by underestimating implicit costs.

3. Avoid Improving a Single Procedure While Ignoring Overall Process Optimization: There is a correlation between each procedure, and defects in a single procedure may originate from problems in the previous procedure. Therefore, reducing scrap cost needs to start from the overall process, optimize the connection between procedures, and avoid "treating the symptoms but not the root cause".

4. Avoid Short-Term Improvement While Lacking Long-Term Persistence: Scrap cost control is a long-term work. A continuous improvement mechanism must be established to continuously optimize processes, improve technologies, and strengthen management. Avoid relaxing control after phased improvement, which may lead to a rebound in the scrap rate.

V.

Scrap cost control in PCB manufacturing is a complex systematic project. Accurately accounting for scrap cost is the premise, clarifying the scrap causes of each procedure is the foundation, systematic control strategies are the core, and sound implementation guarantee is the key. Enterprises need to establish a full-process control system of "source prevention, process control, and terminal improvement" from multiple dimensions such as design, materials, equipment, processes, operations, inspection, and management. By optimizing design to improve process feasibility, strictly controlling material quality to reduce inherent defects, upgrading equipment precision to improve stability, standardizing operation processes to reduce manual errors, strengthening full-process inspection to timely detect defects, and conducting in-depth data analysis for continuous optimization, a dual reduction in scrap rate and scrap cost is achieved.

In the context of increasingly fierce industry competition, reducing scrap cost can not only improve enterprise profitability but also enhance capacity utilization, shorten delivery cycles, and strengthen customer trust, helping enterprises gain market competitive advantages. PCB manufacturing enterprises need to formulate practical control plans according to their own production scale, product types, and process levels, continuously optimize and improve, integrate scrap cost control into every link of production and operation, and realize high-quality and low-cost sustainable development.